City of DeKalb Mayor Cohen Barnes | City of DeKalb, Illinois/Facebook

City of DeKalb Mayor Cohen Barnes | City of DeKalb, Illinois/Facebook

City of Dekalb City Council met June 9.

Here is the agenda provided by the council:

A. CALL TO ORDER AND ROLL CALL

B. PLEDGE OF ALLEGIANCE

C. APPROVAL OF THE AGENDA

D. PRESENTATIONS

1. Presentation of the Final Draft of the FY2024 Annual Comprehensive Financial Report (ACFR).

E. PUBLIC PARTICIPATION

F. APPOINTMENTS

None.

G. CONSENT AGENDA

1. Minutes of the Regular City Council Meeting of May 27, 2025.

2. Accounts Payable and Payroll through June 9, 2025, in the Amount of $4,123,220.88.

3. Investment and Bank Balance Summary through April 2025.

4. Year-to-Date Revenues and Expenditures through April 2025.

5. Crime Free Housing Bureau Report – May 2025.

H. PUBLIC HEARINGS

None.

Assistive services, including hearing assistance devices, available upon request.

I. CONSIDERATIONS

1. Consideration of the State Legislature’s Elimination of the 1% Statewide Tax on Grocery Sales, Effective January 1, 2026.

City Manager’s Summary: Before launching into a detailed discussion of potential local policy options in light of the Illinois Legislature’s elimination of the state 1% grocery tax, effective January 1, 2026, it might be useful to understand the origins of the grocery tax, where it goes, and why.

Background

Until 1989, retailers with multiple Illinois locations were required to file returns with the Illinois Department of Revenue as well as home rule units of government. Sales tax reform in 1989 attempted to relieve this burdensome system by limiting the powers of home rule cities to impose their own sales taxes (except for special taxes relating to Regional Transit Authority costs and obligations). In the grand bargain implemented in 1990, the trade-off for losing local authority was offset by an increase in the general state sales tax rate from 5% to 6.25%.

Additional state enactments since 1990 have further defined the “Retailer’s Occupation Tax” (ROT), or sales tax, which imposes a 6.25% on general merchandise and a 1% tax on qualifying food, drugs, and medical appliances. The 1% tax is charged on most food items for home consumption, or “Food at Home” (FAH), and is often called a “grocery tax.” One percentage point of the state’s ROT (or 16% of state ROT collections) is collected by the state and then passed through to municipal governments. The widely reported elimination of the 1% grocery tax by the Illinois legislature, effective January 1, 2026, would lower ROT revenue by reducing the taxable base of retail sales, although some items such as alcoholic beverages, soft drinks, and prepared food for immediate consumption would continue to be taxed at the 6.25% rate. The authority to implement a 1% grocery sales tax locally by ordinance – for both home rule and non-home rule municipalities – was established by the state 2025 budget legislation (Public Act 103-0781), which was approved during the 2024 Spring Legislative Session. A local grocery sales tax may only be levied at 1%, and not any other increment.

In sum, the elimination of the grocery tax only eliminates the portion of ROT revenue that is generated by grocery sales; it would not eliminate the 1% tax on prescription and non prescription drugs, tobacco, adult-use cannabis, soft drinks, candy, food prepared in a restaurant for take-out or delivery, and grooming and hygiene products. Among the foods that qualify for the grocery tax suspension are deli items sold by weight, fresh fruits and vegetables, meat trays, breads and bagels, items sold in premeasured containers such as ice cream (unless sold in packaged cones or other fashion for immediate consumption), vegetable or fruit juices with more than 50% natural juices, nuts that are not prepared in combination with sugar, infant formula, and protein supplements that do not make a medicinal claim on their labels.

Consumer Impacts

Purchases made with “Supplemental Nutrition Assistance Program” (SNAP) benefits through the Illinois “link card” program cannot be charged the 1% grocery tax. The SNAP program is designed to serve the poorest among us and defines eligible households by reference to 165% of the federal poverty level, which varies according to household size. Effective October 2024, yearly income limits for qualifying Illinois households needed to conform to the following schedule:

| No. in Household* | Maximum Annual

Household Income | Maximum Annual

Household Income if with Over 60 or Disabled Members | Maximum

Monthly/Annual Benefits |

| 1 | $24,852 | $30,120 | $292 / $3,505 |

| 2 | $33,732 | $40,872 | $536 / $6,432 |

| 3 | $42,612 | $51,636 | $768 / $9,216 |

| 4 | $51,480 | $62,400 | $974 / $11,700 |

| 5 | $60,360 | $73,152 | $1,158 / $13,896 |

The DeKalb County SNAP servicing office estimates that in 2024, 12%-13% of DeKalb County households participated in the SNAP program for varying lengths of time. While eligible, Link card recipients receive a “credit” equal to the monthly maximum by household. Recipients are responsible for tracking their monthly spending through their receipts. The grocery tax is not suspended if Link card holders pay with cash or with coupons.

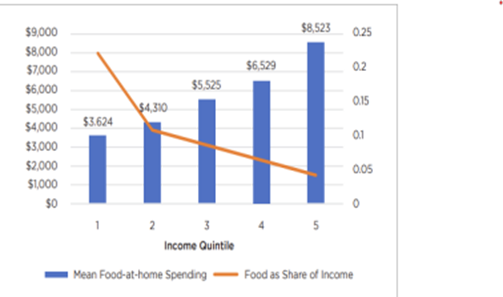

In support of its opposition to the elimination of the grocery tax, the Illinois Municipal League which represents 1294 cities, villages, and towns in Illinois sponsored a study of “Food at Home” (FAH) expenditures as a share of household income about a year ago. The study concluded that the impact of eliminating the grocery tax is not as clear-cut as the sponsors claimed over a year ago. Since the state grocery tax is just 1%, data from the Bureau of Labor Statistics suggest that a low-income family would not realize the “few hundred bucks” in savings in the course of one year that were promised by state-level advocates. The following table shows that average annual expenditures on “Food at Home” in 2022 (the latest available data year) in the United States ranged from $3,624 for the lowest-income households to $8,523 for the highest-income households. It would take a low-income household about 8 years to accumulate several hundred dollars in tax savings from the elimination of the grocery tax. Interestingly, the state grocery tax liability of higher-income households would go down the most due to their higher FAH spending, but even the highest quintile households would need more than 3 years to accrue several hundred dollars in savings.

From a state policy level, there is one more significant finding of note. The Illinois grocery tax is only marginally regressive in practice with respect to the bottom of the income scale. A tax

is regressive when the amount paid is higher relative to household income for lower income households. Accordingly, the important issue is not whether “Food at Home” expenditures are regressive but whether grocery tax payments are. As a means-tested program, SNAP benefits are distributed disproportionately to lower income households, relieving many of them of the grocery tax burden (some SNAP benefits are spent on non-grocery items that are fully taxed). Therefore, to assess the regressivity of the tax, how much “Food at Home” is financed by SNAP program needs to be considered.

The table below shows that the grocery tax is not regressive with respect to the lowest quintile of incomes, but is slightly regressive in terms of household income quintiles 2 and 3*:

| Income

Quintile Lower Limit | Mean

Income | Average

FAH Expenses | Average

FAH Purchased with SNAP | Taxable

FAH Spending | Average

Grocery Tax | Tax as

Share of Income |

| $0 | $14,191 | $3,624 | $3,459.92 | $164.08 | $1.64 | 0.01% |

| $25,807 | $37,441 | $4,310 | $1,346.74 | $2,963.26 | $29.63 | 0.08% |

| $50,092 | $65,659 | $5,525 | $405.12 | $5,119.88 | $51.20 | 0.08% |

| $83,696 | $108,730 | $6,529 | $60.22 | $6,468.78 | $64.69 | 0.06% |

| $140,363 | $244,025 | $8523 | $0.00 | $8,523.00 | $85.23 | 0.04% |

Further, the federal Bureau of Labor Statistics data show that “Food at Home” expenditures decline as household incomes rise (and families seek more meals in restaurants). In 2022, families in the lowest 20% of the income distribution scale spent 26% of their income on “Food at Home,” and families at the highest quintile spent 3.5% of after-tax income on FAH.

Finally, it should be noted that whatever a municipality chooses to do with respect to the grocery tax, the State of Illinois will actually make some money on the process. The current tax is a pass-through, so its elimination is no loss to the State of Illinois. If a home rule community opts to impose a 1% grocery tax to replace the tax removed by the state on January 1, 2026, the grocery tax will continue to be collected by the state and remitted to the home rule community, after a 3% administrative processing fee is imposed.

Fiscal Impacts for the City of DeKalb

As the DeKalb City Council considers whether to implement an identical 1% tax once the state 1% tax is removed at the end of this calendar year, a primary consideration in addition to the economic data noted above is the fiscal impact on general operations. In 2024, the 1% grocery tax produced $795,356 for the City of DeKalb. The tax proceeds are reported as one of several sales and use tax entries in the City’s General Fund, which is the principal source of revenue for the City’s operating departments. The 1% grocery taxes were derived from $79,535,585 in actual sales.

Sales and use taxes are the largest category of General Fund revenues. In the 2025 General Fund budget, sales and use taxes make up 33.35% ($17,010,908) of all budgeted General Fund revenues ($51,002,166). The next largest General Fund revenue category is the Fire and Police pension levies (16.35%) which are necessary to meet the City’s current obligations but cannot be used to offset salaries and wages, commodity purchases, or contractual services. Personnel expenditures make up 79% of all operating expenditures in 2025; the other allocations are for debt service (0.9%), small capital equipment purchases (0.3%), contractual services (8.7%), commodities (2.1%), and transfers to other City funds (8.9%).

If a local 1% grocery tax did not replace the 1% statewide tax, effective January 1, 2026, the overall sales and use tax revenue stream would be reduced by 5% ($795,356/$17,010,908). A 5% reduction in the largest revenue stream supporting City operating departments will almost certainly lead to cuts in operating expenditures. In the COVID years, the City froze all new hires and did not fill open positions created by retirements or transfers to other employment. To maintain Council objectives and a constant level of operating services in those years, ARPA assistance was necessary. No such assistance from the state government to offset municipal revenue losses has been offered. Other options might include the following: (1) reductions in General Fund transfers to other funds (e.g. the large transfer from the general operating fund to Fund 400 for street maintenance), or (2) a freeze on unspent allocations to local social service agencies participating in the City’s annual Human Services grant program (much of the $225,000 has not yet been spent). Neither of these two options is recommended.

Recommendation

The City’s 1% grocery tax proceeds are not derived from the community’s poorest households who qualify for supplemental nutrition assistance. One might argue that the City should focus on working poor families whose household income exceeds the qualifying thresholds in the statewide SNAP program, but there is no generally accepted methodology in Illinois government circles that defines logical “tax forgiveness” parameters for households living above the SNAP program strata.

Since October 2024, City polling has identified over 50 municipal governments which have identified their intention to approve a local 1% grocery tax, effective January 1, 2026:

Batavia, N. Aurora, Carol Stream, Des Plaines, Lake Zurich, Algonquin, Schaumburg, Wheaton, Elk Grove, Buffalo Grove, Lombard, Wheeling, Palatine, Burlington, Peoria, Normal, Berwyn, Blue Island, Chicago Heights, Cicero, Crestwood, Forest View, Harwood Heights, Hoffman Estates, Lyons, Markham, Melrose Park, Morton Grove, Norridge, Oak Lawn, Orland Park, River Forest, South Barrington, Tinley Park, Pontiac, East Dundee, Edwardsville, Washington, Pekin, Pontiac, Carbondale, Danville, Clarendon Hills, Elgin, Yorkville, Sugar Grove, South Elgin, Elburn, Pingree Grove, St. Charles, Sleepy Hollow, Genoa, and Sycamore.

As described above, the impact of eliminating the 1% tax on “Food at Home” purchases for DeKalb’s neediest families is possibly $50 in one year. The reduction of the City’s operating revenues by approximately $800,000 will have a significant impact on personnel services provided by the City’s public safety departments.

The City Manager recommends the approval of a local 1% grocery tax, effective January 1, 2026. If the City Council concurs, an appropriate ordinance can be brought to the next Council meeting. A decision on this critical issue needs to be made before the preliminary General Fund revenue and expenditure goals are prepared in July in advance of the Joint City Council/Finance Advisory Board meeting in mid-August.

2. Consideration of Whether or Not to Include “Vape Vending” in Locally Licensed Bars.

City Manager’s Summary: Since early March of this year, out-of-town vendors have inquired about City codes that might bear on what are known as “vape vending” machines. Such machines (see picture that follows) allow customers 21 years of age or older to use credit cards to purchase packets from vending machines that provide the user a smoke-based inhalant. Presently, such machines do not explicitly fit the description of vending machines permitted in bars, as defined in Chapter 64 “Smoking Regulations”, Section 64.17, “Vending Machines,” of the DeKalb Municipal Code, although tobacco-based products can be purchased from vending machines in establishments with a Bar liquor license as well as “non profit entities” (e.g. clubs) with a PENP (Public Entity/Non-Profit) license.

Based on recent Council concerns about the proliferation of stores selling tobacco products and also the potential adverse health impacts of various types of chemical inhalants, the City Staff have interpreted the provisions of Section 64.17 of the Municipal Code to exclude vape vending machines.

City Council direction about the propriety of licensing vape vending machines is requested.

3. Consideration of Whether or Not to Permit the Sale of Unregulated Hemp-Derived THC (Tetrahydrocannabinol) Products in the City of DeKalb.

City Manager’s Summary: Hemp and marijuana are variants of the cannabis plant, but hemp naturally contains smaller traces of THC, the main psychoactive ingredient of cannabis plants. Federal law defines hemp as an agricultural product with no more than 0.3 percent THC in dry weight. At this low dose, the hemp products are unregulated and can be sold as edibles or pre-rolled joints without quality testing and outside dispensaries which are licensed and heavily taxed by state and local laws.

In DeKalb, several stores which sell tobacco products are also openly selling jars of rough cut hemp which can be ground, rolled and smoked. This retail practice, presently legal, has confused customers. On several occasions, the DeKalb Police Department has purchased such products and sent them for lab testing which has indicated that in their unadulterated form they are within the 0.3 percent THC limit.

According to media reports, the possibility that hemp that can produce a “high” has come under increasing media attention. Through a loophole in the 2018 Farm Bill, which aimed to help farmers grow industrial hemp, enterprising consumers can buy legal hemp in bulk, and extract and concentrate the THC ingredient. Although licensed dispensaries track their products from “seed to sale” to assure they have been tested for pesticides, mold, metals and adulterants, no such requirements apply to hemp. Since 2023, the U.S. Food and Drug Administration – slow to act avoid the curtailment of legal sales – has increased its investigation of complaints about inadequate or confusing labeling that can result in children or unsuspecting adults ingesting harmful doses of unregulated edible food products containing THC. A particularly worrying trend is the merchandising of products that bear a strong resemblance to popular snacks and candies. Copycat products are being sold in disposable foil packages with such names as “Cookie Cat Crunch,” “Infused Sour Slizzles,” and “Flamin’ Hot Cheetos.”

The question before the Council is whether or not to do one of the following:

a. Take no action.

b. Suspend the sale of ingestible or inhalable hemp products.

c. Ban the sale of ingestible or inhalable hemp products.

City Council direction is recommended.

J. RESOLUTIONS

1. Resolution 2025-063 Receiving and Filing the FY2024 Annual Comprehensive Financial Report (ACFR), Single Audit Report, Report on Compliance With Public Act 85-1142 (TIF Report), Downstate Operating Assistance Certification And Independent Auditor’s Reports, Illinois Grant Accountability And Transparency Act – Consolidated Year-End Financial Report (CYEFR), and Management Letter.

City Manager’s Summary: The following reports were produced under the supervision of Brian LaFevre, a principal with Sikich CPA LLC. Collectively, they constitute the final draft of the independent audit of the City’s finances for the fiscal year ended December 31, 2024:

▪ Annual Comprehensive Financial Report (ACFR)

▪ Single Audit Report

▪ Report on Compliance with Public Act 85-1142 (TIF report)

▪ Downstate Operating Assistance Certification and Independent Auditor’s Reports

▪ Illinois Grant Accountability and Transparency Act (GATA) – Consolidated Year End Financial Report (CYEFR)

▪ Management Letter

The ACFR is the primary report generated as a result of the annual audit, and encompasses all funds and operations of the City, including the Police Pension and Firefighter’s Pension Funds, and the DeKalb Public Library (as a discretely presented component unit). A synopsis of that report is detailed below.

The single audit report contains information on all the federal grant programs administered by the City during fiscal year 2024.

The Report on Compliance with Public Act 85-1142 contains information on the operations of TIF #3. TIF #1 expired on December 31, 2021, and the small fund balance amount that remained was transferred to TIF #3 on December 31, 2023.

The Downstate Operating Assistance Certification and Independent Auditor’s Reports is an audit of one specific City grant program of the Mass Transit Fund. The reports are prepared for the grant year, which ended June 30, 2024.

The Consolidated Year-End Financial Report (CYEFR) is a requirement of the Illinois Grant Accountability and Transparency Act (GATA), which was previously included as a supplemental schedule within the ACFR. The report provides expanded details on the City’s state, federal, and other grant expenditures during the fiscal year.

The Management Letter discloses any instances of material weaknesses in the City’s internal control identified during the audit (there were no such instances for FY 2024). The City must be audited annually in accordance with state statutes. The independent audit firm of Sikich LLP conducted the audit of the City of DeKalb for the fiscal year ending December 31, 2024. Sikich LLP issued an unmodified (“clean”) opinion on the City’s financial statements, which is the highest opinion level an entity can receive.

The General Fund’s actual excess of total revenues over (final) 2024 budget was approximately $698,849. Actual FY 2024 expenditures and transfers out were $48,786,057 or $502,188 below the amended budgeted FY 2024 expenditures. As a result, the General Fund balance ended at $35,715,931, a positive change in fund balance of $3,771,812.

| Final

Original (Amended) General Fund Budget Budget Actual Revenues Taxes 24,434,086 24,999,231 24,666,506 Licenses and Permits 867,866 867,866 679,402 Intergovernmental* 17,885,487 17,885,487 18,525,223 Charges for Services 4,569,905 4,569,905 4,688,647 Fines and Forfeitures 494,920 494,920 514,345 Investment Income 400,000 1,615,829 1,615,827 Miscellaneous 364,394 364,394 634,739 Total $ 49,016,658 $ 50,797,632 $ 51,324,689 Expenditures General Government $ 7,032,914 $ 7,032,914 $ 6,818,358 Public Safety 32,298,977 32,298,977 32,491,087 Highways and Streets 3,607,271 3,607,271 3,225,158 Community Development 1,371,199 1,371,199 1,295,678 Debt Service - - 28,829 Total $ (44,310,361) $ (44,310,361) $ (43,859,110) Transfers In 779,500 779,500 779,500 Transfers (Out) (2,198,497) (4,698,497) (4,698,497) Sale of Capital Assets 2,500 2,500 225,230 Lease Liability Proceeds Change in Fund Balance $ 3,289,800 $ 2,570,774 $ 3,771,812 |

EAV 2015 – 2024

Extraordinary political constraints imposed by Illinois Governor Pritzker to combat the COVID 19 pandemic led to severe business interruption in 2020. Despite uncertainty of revenue recovery in 2021, and a recession in 2022, the other major revenue sources of the City (1.0% municipal sales tax, 1.75% home rule sales tax and state income tax) experienced considerable gains in 2023 and continued to hold strong in 2024 as depicted below.

COMBINED MUNICIPAL & HOME RULE SALES TAX 2016 – 2024

*The City changed its fiscal year end to December 31, 2016, and this represents July 1 – December 31, 2016.

In 2024, combined sales tax revenues increased slightly by 0.5% over 2023. The City has a healthy mix of retailers providing grocery and household goods, home improvements, pharmaceuticals, clothing, auto dealerships and restaurants. Online retailers also contributed to the tax base.

DEKALB’S SHARE OF ILLINOIS INCOME TAX PROCEEDS, 2016 – 2024 *The City changed its fiscal year end to December 31, 2016, and this represents July 1 – December 31, 2016.

Income taxes experienced an increase of 6.3% from 2023 to 2024. The State of Illinois remits income tax on a per capita basis, and the Illinois Municipal League tracks and forecasts this revenue source. For calendar year 2023, the actual distribution was $155.85/per capita; for calendar year 2024 it was $160.87, an increase of $5.02. The other factor impacting this revenue source was the certification of the City’s population from the 2020 census: the City’s population declined from 44,030 to 40,290. This became effective with December 2021 remittances and the impact was fully felt in FY 2022.

The revenue sources described above are expected to remain stable or increase in future years due to continued economic development, and the City will continue to analyze these sources annually to ensure that expenditures do not outpace the anticipated revenues.

The Fund Balance Policy requires that the General Fund’s unassigned fund balance be maintained at a minimum level equal to 25% of annual expenditures to provide financing for unanticipated expenditures and revenue shortfalls and possible delays and changes in state distribution of shared revenues. For FY 2024, the City has again achieved this marker with an unassigned fund balance of $35,715,931 representing 73.2% of annual expenditures, including transfers. The overall change in fund balance was an increase of almost $3.8 million (12%) over the prior year.

Additionally, the Fund Balance Policy requires that the Water Operating Fund’s unrestricted net assets be maintained at a minimum of 25% of annual budgeted operational expenses. For FY 2024, the City has achieved this requirement with unrestricted net assets totaling 25% of annual budgeted operating expenses.

For the City’s other funds, the table below summarizes the changes during fiscal year 2024:

| Beginning Revenues & Expenditures & Ending

Fund Fund Balance Transfers In Transfers Out Fund Balance Mass Transit $ 3,221,269 $ 11,554,753 $ 11,106,570 $ 3,669,452 Motor Fuel Tax 2,597,927 3,622,162 5,479,621 740,468 Capital Equip Replace 509,576 875,242 982,191 402,627 Water* 34,884,194 8,255,623 6,641,544 36,498,273 Airport 31,415,857 1,625,494 1,438,324 31,603,027 Capital Projects 845,715 1,925,428 1,849,332 921,811 GEMT 1,480,818 1,279,318 1,400,230 1,359,906 Station 4 Construction 4,307,979 200,506 2,707,535 1,800,950 ARPA 156,690 48,853 12,657 192,886 EAP - 50,000 - 50,000 Foreign Fire Ins. Tax 87,851 101,536 77,053 112,334 Housing Rehab 62,613 4,208 3,753 63,068 CDBG - 281,818 281,818 - SSA #3 1,995 1,034 1,531 1,498 SSA #4 8,051 5,686 2,734 11,003 SSA #6 21,900 12,482 10,573 23,809 SSA #14 13,733 2,284 1,340 14,677 SSA #29 78,814 51,468 5,599 124,683 SSA #30 71,992 52,103 - 124,095 TIF #3 1,668,293 1,031,339 678,172 2,021,460 Debt Service 135,055 1,999,575 1,999,722 134,908 Refuse (212,872) 2,599,465 2,525,042 (138,449) Workers Comp/Liab 1,487,818 1,504,055 1,451,202 1,540,671 Health Insurance 1,466,520 7,303,516 6,676,451 2,093,585 Police Pension 49,874,585 9,798,789 4,987,530 54,685,844 Firefighter's Pension 40,062,912 10,054,895 4,959,696 45,158,111 |

*Consists of Water Operating, Water New Construction, and Water Capital.

As of December 31, 2024, the City had a total of $154,724,186 in long-term debt and obligations outstanding, of which $106,818,314 consisted of net pension liabilities and $13,575,000 consisted of general obligation bonds. The table that follows summarizes the City’s bonded and other indebtedness, with the totals on December 31, 2024, and December 31, 2023, depicted for comparison sake.

| Governmental Business-Type

Activities Activities Total Total 2024 2023* 2024 2023* 2024 2023* General Obligation Bonds $ 13,575,000 $ 15,225,000 $ - $ - $ 13,575,000 $ 15,225,000 Premium on Bonds 183,839 201,028 $ - - 183,839 201,028 Installment Contracts 251,081 412,416 30,086 69,303 281,167 481,719 Lease Liabilities 230,838 333,924 56,298 78,771 287,136 412,695 IEPA Loans - - 665,117 711,937 665,117 711,937 Compensated Absences Payable* 5,994,637 5,434,550 359,721 362,200 6,354,358 5,796,750 Net Pension Liability 105,987,512 111,044,837 830,802 1,006,727 106,818,314 112,051,564 Total OPEB Liability 24,904,561 26,834,848 807,141 817,672 25,711,702 27,652,520 Claims Payable 397,553 470,644 - - 397,553 470,644 Asset Retirement Obligation - - 450,000 450,000 450,000 450,000 Total $ 151,525,021 $ 159,957,247 $ 3,199,165 $ 3,496,610 $ 154,724,186 $ 163,453,857 |

As no anticipated changes are expected, acceptance of this final draft is recommended.

2. Resolution 2025-064 Approving a Restaurant-Full Liquor License for Florentino’s Charhouse LLC at 106 E. Lincoln Highway.

City Manager’s Summary: The owners of Florentino’s Charhouse (Florentino Castro Arellano, Salvador Castro Arellano, and Alfredo Castro Arellano) have submitted an application for a Restaurant-Full liquor license. If approved, the license will be considered “conditional” until the requirements laid out in the attached resolution are met, which includes receipt of a State of Illinois liquor license. The City will receive an initial issuance fee of $5,659 if the license is approved. Non-refundable fees for the liquor license application, Fire Life Safety application, and background investigations in the amount of $766 have been paid. The licensing term for a Restaurant-Full liquor license begins on May 1 and ends on April 30 with an annual renewal fee of $3,735. Background investigations for all three owners have been approved by the DeKalb Police Department.

City Council approval of the license is recommended, subject to the conditions described in the resolution.

3. Resolution 2025-065 Authorizing a Professional Services Agreement with Civil Engineering Services, Inc.

City Manager’s Summary: Since the resignation of Zac Gill as city engineer, effective April 4, the City’s oversight of multiple engineering projects has been assumed on an interim basis by C.E.S Engineering of Belvidere, Illinois. The firm’s founder and president, Kevin Bunge, has generously assisted the City staff several days a week, or more often as needed, while the search for a full-time replacement continues. C.E.S. Engineering is on the City’s preferred list of engineering consulting firms. By coincidence, the firm was not currently assigned a major City contract this Spring that would have posed a conflict in terms of overall supervision.

In recent weeks, Mr. Bunge has worked with Fehr Graham and WBK Engineering, in particular, on a number of approved contracts for construction inspection such as the $4.5 million annual street maintenance program and the Normal Road roundabout, as well as the very preliminary engineering for a N. First Street roundabout. He has also provided valuable counsel on engineering questions that are under staff review every week, ranging from grading designs for new developments to neighborhood storm water drainage issues.

Under the City Manager’s spending authority of $20,000, Mr. Bunge has been very flexible and responsive, although his own substantial firm makes daily demands on his time. While the current search for a permanent replacement engineer continues, his hourly compensation will likely exceed the City Manager’s authority. The search for a permanent in-house engineer has not yet offered any certainty as to the time that a permanent engineer will begin his or her duties. Accordingly, the City Manager is seeking City Council authority to enter a new contract with industry charge-out rates as specified in the attached addendum.

City Council approval is recommended.

4. Resolution 2025-066 Authorizing Supplemental FY2025 Human Services Funding.

City Manager’s Summary: At the last regular Council meeting of May 27, the City Council considered a proposal to implement a “supplemental human services” grant program with the following features:

a. A supplemental General Fund allocation of an additional $75,000 to bring the overall FY2025 human services funding to $300,000.

b. The mailing of applications for supplemental funding to those agencies that applied and were granted some level of human service funding in late January 2025 (23 in all).

c. A scoring metric to establish eligibility and levels of funding with a preference for meeting basic needs such as housing, food, and care for the elderly and disabled.

d. As with the core grants issued in January of each year, this supplemental funding round would be reviewed and scored by members of a seven-member City review team led by Jennifer Yochem, the City’s Community Services Coordinator. The grant requests and the review group’s consensus recommendations would then be considered by the City Manager in advance of bringing them to the Council for final action.

In its first year (FY1998), human services grants totaled $184,000. The total budgeted amount was increased to $200,000 in FY2022 and to $225,000 in FY2024. If approved, the supplemental $75,000 would bring the 2025 program to $300,000. Funding for this initiative will be drawn from the FY2025 General Fund balance.

City Council approval is recommended.

5. Resolution 2025-067 Authorizing the Award of a Contract to Tri-R Systems Inc. to Upgrade the Supervisory Control and Data Acquisition (SCADA) System in an Amount Not to Exceed $606,000, with Staff Authority to Approve Change Orders up to $666,600.

City Manager’s Summary: The Water Division is seeking Council approval to authorize the purchase and implementation of a Supervisory Control and Data Acquisition (SCADA) system to modernize the monitoring and control infrastructure at the City’s water treatment facilities. Such an upgrade was budgeted in the amount of $505,000 in the FY2025 Budget for the Water Capital Fund (Fund 620, Line Item 620-00-00-86100).

Several key considerations have prompted this initiative. First, the current technology is dated and no longer supported. Second, new technologies are available which will improve the water system’s reliability and provide further protection against ransomware attacks.

Justin Netzer, Water Superintendent, and his staff pursued proposals for the replacement of the existing system. Two proposals were received:

| Base Bid | Option 1 | Option 2 | Total Bid | |

| Tri-R Systems | $560,000 | $25,000 | $21,000 | $606,000 |

| Concentric | $708,600 | $32,700 | $5,100 | $746,000 |

To accommodate potential cost increases related to tariffs and other unforeseen expenses, the Water Division staff further recommend including a 10% contingency of $66,600, bringing the total authorized expenditure to an amount not to exceed $666,600. While Superintendent Netzer does not anticipate exceeding the total contract amount of $606,000, the added contingency ensures financial flexibility to address any unexpected challenges that may arise during the project.

City Council approval is recommended. The appropriate increase in the 620-00-00-86100 budget will be made as FY2025 amendments are brought to the Council for review and approval in the next several months.

6. Resolution 2025-068 Authorizing the Award of a Contract to West Side Tractor Sales Company for the Purchase of Snow Removal Equipment and Authorizing a Professional Services Agreement with Crawford, Murphy and Tilly, Inc. for Design Engineering Services in an Amount Not to Exceed $602,254.48, with a Local Share Not To Exceed $60,225.48.

City Manager’s Summary: In June 2019, Governor J.B. Pritzker signed the bipartisan Rebuild Illinois capital bill, providing Illinois with its first capital infrastructure plan in decades. As part of this initiative, $150 million was allocated for projects at airports across the state to promote safe and efficient operations and to support economic development opportunities throughout Illinois.

DeKalb Taylor Municipal Airport was awarded funding through the Illinois Department of Transportation (IDOT) to purchase snow removal equipment under this program. The acquisition of this new equipment will significantly improve the airport’s ability to remove snow efficiently, enhancing operational safety during winter months.

The total grant funding allocation for the project is $585,000 (90%) provided by IDOT and $65,000 (10% local match) will need to be contributed by the City of DeKalb for a total of $650,000. The IDOT project number is known as “DKB-4906 – Acquisition of Snow Removal Equipment.”

From April 9 to May 9 of this year, bids were invited for the following equipment:

▪ One (1) Wheel Loader with Bucket

▪ One (1) Wheel Loader Broom Attachmen

▪ One (1) Skid-Steer Loader

▪ One (1) Skid-Steer Loader Broom Attachmen

▪ One (1) Skid-Steer Loader Box Plow Attachment

▪ One (1) 84-inch Snow Blower for Skid-Steer

The City of DeKalb received two complete bid submissions in response to this solicitation: a. Alta Construction Equipment Illinois, LLC

▪ Base Bid: $577,617.00

▪ Additive Alternate #1 (84" Snow Blower): $22,466.00

▪ Total with Alternate #1: $600,083.00

b. West Side Tractor Sales Co.

▪ Base Bid: $565,609.75

▪ Additive Alternate #1 (84" Snow Blower): $16,547.39

▪ Total with Alternate #1: $582,157.14

After review and evaluation of the submitted bids by the Public Works staff and the engineering consulting firm of Crawford, Murphy & Tilly, West Side Tractor Sales Co. was determined the lowest responsible bidder.

The City Manager recommends the award of the contract to West Side Tractor Sales Co. in the amount of $582,157.14. In addition, for the related design engineering work of Crawford, Murphy & Tilly and their prospective grant closeout reporting expected to be $20,000 plus advertising costs, an additional award of $20,097.34 is requested. The total project cost is $602,254.48 including the base bid and alternate #1.

City Council approval is recommended. The funding will come from Line item 650-00-00- 83900.

K. ORDINANCES – SECOND READING

None.

L. ORDINANCES – FIRST READING

1. Ordinance 2025-026 Authorizing an Amendment to the Special Use Permit Approved by Ordinance 2023-021 in Order to Extend the Timeframe for a Modular Classroom to Remain on the Site at 1133 N. Thirteenth Street (Littlejohn Elementary School).

City Manager’s Summary: As Planning Director Dan Olson writes in his background memorandum, DeKalb Community Unit School District No. 428 is requesting approval of a petition to amend the Special Use Permit approved by Ordinance 2023-021 to extend the time frame for a modular classroom to remain on the site at Littlejohn Elementary School (1133 N.

Thirteenth Street) for three more years. In 2001, the City initially granted a special use permit to the School District for the placement of a modular classroom in the same general location. The modular classroom was removed in about 2011, but the School District petitioned to have a modular classroom placed back on the site in 2017. The school was constructed in 1954.

On July 10, 2017, the City Council approved Ordinance 2017-031 to allow for the addition of a modular classroom just to the west of the existing school building. The ordinance had a three-year time limit. In 2020, as the time limit approached, the City Council approved a three year extension for the modular classroom. In 2023 the City approved Ordinance 2023-021, which granted another two-year extension for the modular classroom. The 2023 Ordinance noted the modular classroom must be removed from the school property by August 15, 2025. The School District plans to replace the current modular classroom this summer with a new unit which will provide a vestibule and bathroom which the current one does not have. The new modular unit would be placed in the same location as the existing one.

The summary provided by the School District states the K-5 enrollment at Littlejohn Elementary was approximately 291 students in the 2024/2025 school year with a capacity of approximately 263 students based on current space and program restrictions. The School District indicates they intend to reduce class sizes district-wide from 28 to 25. Even with this reduction, the School District says that based on current enrollment and the Two-Way Dual Language Program, the modular classroom at Littlejohn Elementary is still needed.

The Planning and Zoning Commission held a public hearing regarding the amendment to the special use permit at their meeting on June 2, 2025. By a vote of 4 to 0 (Becker and Maxwell were absent) the Commission recommended City Council approval of an amendment to Ordinance 2023-021 to extend the time frame for a modular classroom at 1133 N. 13th Street (Littlejohn Elementary School) subject to the condition that the modular classroom may remain on the subject site up to August 15, 2028 and shall be removed from the property, on or before said date. At such time, the surface beneath the modular classroom must be restored to a grassy condition.

City Council approval of the Planning & Zoning Commission recommendation is requested.

2. Ordinance 2025-027 Amending Chapter 51 “Traffic”, Schedule C “Parking Prohibited”, to Establish a No Parking Zone in the 200 and 300 Block of Ridge Drive.

City Manager’s Summary: As Andy Raih writes in his background memorandum, the 2025 Street Maintenance Program includes the addition of traffic-calming islands on Ridge Drive to enhance pedestrian safety, particularly in the vicinity of Jefferson Elementary School. This initiative requires some revisions to Chapter 51, Schedule C of the DeKalb Municipal Code. The following language identifies the prohibited parking:

▪ Ridge Drive, No Parking Any Time, Tow Zone, south side, from a point 100 feet west of the west right-of-way line of Huntington Road to a point 115 feet east of the east right-of-way line Huntington Road.

▪ Ridge Drive, No Parking Any Time, Tow Zone, north side, from a point 100 feet west of the west right-of-way line of Huntington Road to a point 115 feet east of the east right-of-way line Huntington Road.

City Council approval is recommended. M. REPORTS AND COMMUNICATIONS

1. Council Member Reports.

2. City Manager Report.

N. EXECUTIVE SESSION

None.

O. ADJOURNMENT

https://www.cityofdekalb.com/AgendaCenter/ViewFile/Agenda/_06092025-2707

Alerts Sign-up

Alerts Sign-up